The approval of a gene therapy treatment for genetic hearing loss represents a significant milestone in the evolution of modern medicine. It demonstrates how advancements in genetic science, biotechnology, and regulatory innovation are accelerating the commercialization of next-generation therapies that were once considered experimental.

For decades, genetic hearing loss has largely been managed through assistive technologies such as hearing aids and cochlear implants. While these solutions improve quality of life, they do not address the underlying genetic causes of hearing impairment. Gene therapy changes this approach by targeting the root biological mechanism responsible for the condition.

This regulatory approval signals more than just a medical breakthrough. It highlights a broader transformation occurring across the healthcare and biotechnology industries where gene therapies are moving from research pipelines into commercial reality.

As the genetic medicine market expands, competitive advantage will increasingly depend on three critical factors: regulatory speed, manufacturing scalability, and market access. Companies that establish strong commercialization infrastructure early may position themselves as long-term leaders in one of the fastest-growing segments of the life sciences industry.

The Growing Momentum Behind Gene Therapy

Gene therapy has emerged as one of the most promising areas in modern healthcare. Instead of treating symptoms, these therapies aim to correct or replace defective genes responsible for disease development.

This approach has the potential to transform treatment strategies across multiple therapeutic areas including rare diseases, inherited disorders, oncology, ophthalmology, neurology, and metabolic conditions.

Historically, gene therapies faced major challenges related to safety concerns, delivery mechanisms, manufacturing complexity, and regulatory uncertainty. However, advances in vector engineering, genomic research, and clinical trial design have significantly improved the viability of genetic medicines.

The approval of a therapy targeting genetic hearing loss demonstrates growing regulatory confidence in these technologies and reflects the increasing maturity of the gene therapy ecosystem.

For patients and healthcare providers, this opens the possibility of more personalized and potentially curative treatment options. For the biotechnology sector, it confirms that genetic medicine is becoming a commercially sustainable market category rather than a niche experimental field.

Why This Approval Matters

Hearing loss affects millions of individuals worldwide, with a significant portion linked to inherited genetic mutations. Traditional treatment approaches often focus on symptom management rather than biological correction.

Gene therapy introduces a fundamentally different model by addressing the molecular cause of hearing impairment directly within affected cells.

The significance of this approval extends beyond the hearing loss indication itself. It establishes a precedent for future therapies targeting genetic disorders and strengthens industry confidence in the regulatory pathway for genetic medicine products.

Several important implications emerge from this milestone:

- Increased investor confidence in gene therapy platforms

- Greater momentum for rare disease innovation

- Stronger regulatory support for advanced therapies

- Expanded commercial opportunities in precision medicine

- Faster development timelines for next-generation treatments

The approval also demonstrates how regulatory agencies are adapting frameworks to support innovative therapies for unmet medical needs. Accelerated pathways, priority review programs, and specialized incentives are helping reduce barriers for advanced biotechnology products entering the market.

This shift is creating a more competitive environment where execution speed becomes increasingly important.

Regulatory Speed as a Competitive Advantage

In the emerging genetic medicine market, regulatory strategy is becoming a core business differentiator.

Companies that can efficiently navigate clinical development, regulatory submissions, and approval processes may gain significant first-mover advantages. Early approvals often create opportunities to establish physician relationships, build patient trust, and secure market share before competitors enter the space.

Regulatory agility is particularly important in gene therapy because these products often target rare or highly specialized conditions where patient populations are limited.

Organizations with strong regulatory expertise can:

- Accelerate clinical timelines

- Optimize trial design

- Improve approval probability

- Reduce commercialization delays

- Strengthen investor confidence

As competition increases, regulatory capabilities may become just as valuable as scientific innovation itself.

Biotechnology firms are increasingly investing in integrated regulatory teams, strategic partnerships, and global compliance frameworks to support faster product development and international expansion.

For consulting and advisory organizations, this creates growing demand for regulatory intelligence, market entry strategy, and commercialization planning services within the advanced therapy sector.

Manufacturing Scalability Will Define Market Leaders

While scientific discovery remains essential, manufacturing scalability is becoming one of the largest operational challenges in gene therapy commercialization.

Unlike traditional pharmaceutical products, gene therapies involve highly complex manufacturing processes that require precision, consistency, and strict quality control. Production often includes viral vector engineering, cell processing, cold-chain logistics, and advanced biomanufacturing infrastructure.

Scaling these operations commercially is expensive and technically demanding.

As more therapies receive approval, companies capable of building scalable and reliable manufacturing systems may gain substantial competitive advantages.

Manufacturing scalability impacts several critical business areas:

- Product availability

- Treatment cost

- Global market expansion

- Supply chain resilience

- Regulatory compliance

- Long-term profitability

Many biotechnology companies are now prioritizing manufacturing partnerships, capacity expansion, and process automation to prepare for increased market demand.

The industry is also seeing rising investment in contract development and manufacturing organizations (CDMOs) specializing in advanced therapies. These partnerships allow smaller biotech firms to accelerate commercialization without building large-scale manufacturing facilities independently.

Over time, manufacturing efficiency may become one of the defining factors separating commercially successful gene therapy companies from those that struggle to scale operations.

Market Access and Reimbursement Challenges

Despite strong clinical potential, market access remains one of the most complex aspects of gene therapy commercialization.

Many genetic medicines involve exceptionally high development costs and often carry premium pricing structures due to their specialized nature and limited patient populations.

Healthcare systems, insurers, and payers must determine how to evaluate long-term therapeutic value while managing financial sustainability.

This creates a challenging environment where companies must demonstrate not only clinical effectiveness but also economic value.

Successful commercialization strategies increasingly require:

- Strong health economics data

- Outcomes-based pricing models

- Reimbursement planning

- Patient access programs

- Stakeholder engagement strategies

Companies that proactively address market access challenges early in development may improve adoption rates and commercial performance after approval.

This is especially important as more gene therapies enter the market and competition for reimbursement support intensifies.

The Future of Genetic Medicine

The approval of gene therapy for hearing loss represents another step toward a broader transformation in healthcare where treatments become increasingly personalized, targeted, and biologically precise.

Over the next decade, advancements in gene editing, AI-driven drug discovery, genomic sequencing, and biotechnology manufacturing are expected to accelerate the expansion of genetic medicine across multiple disease categories.

As innovation continues, competitive advantage will depend on far more than scientific discovery alone.

The companies most likely to lead this market will be those capable of combining:

- Scientific innovation

- Regulatory execution

- Scalable manufacturing

- Commercial readiness

- Strategic market access planning

For healthcare organizations, investors, and biotechnology leaders, the message is clear: genetic medicine is evolving into a major commercial healthcare sector with long-term global impact.

Organizations that invest early in regulatory expertise, operational scalability, and commercialization capabilities may be best positioned to shape the future of precision medicine.

Industry Overview

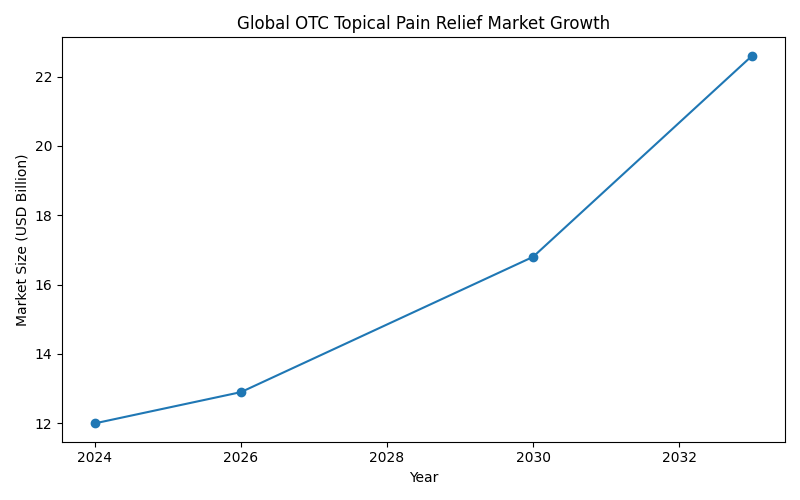

The global topical pain relief market is projected to grow significantly over the next decade, driven by increasing chronic pain conditions, aging populations, and rising self-care awareness.

Global Market Growth Projection

| Year | Market Size (USD Billion) |

|---|---|

| 2024 | 12.0 |

| 2026 | 12.9 |

| 2030 | 16.8 |

| 2033 | 22.6 |

Market Growth Graph

Key Growth Drivers

- Increasing arthritis and joint pain cases

- Rising sports-related injuries

- Aging global population

- Consumer preference for non-invasive treatment

- Higher awareness of self-medication

- Expansion of e-commerce healthcare channels

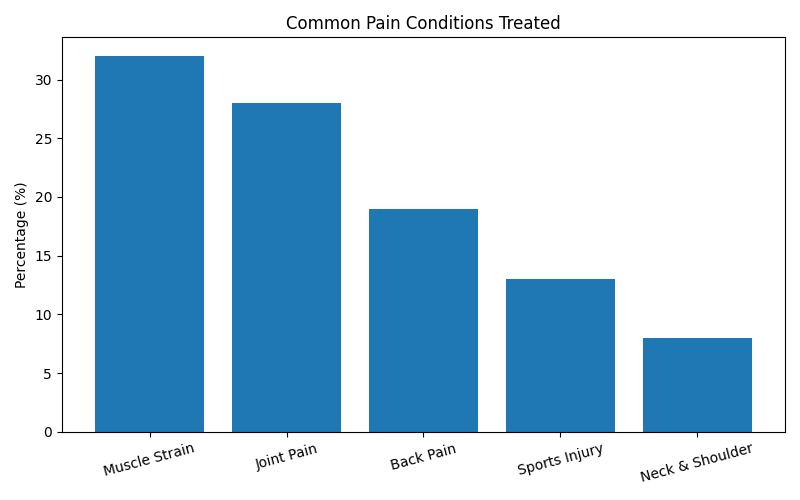

Clinical & Consumer Pain Landscape

Musculoskeletal pain remains one of the most common health complaints worldwide. Consumers increasingly prefer topical OTC therapies because they offer:

- Rapid localized relief

- Reduced gastrointestinal side effects

- Lower systemic exposure

- Convenient application

- Improved patient compliance

Scientific literature supports the efficacy of topical analgesics for musculoskeletal pain management.

Most Common Pain Conditions Treated

| Pain Condition | Consumer Share (%) |

|---|---|

| Muscle Strain & Sprain | 32% |

| Joint Pain & Arthritis | 28% |

| Back Pain | 19% |

| Sports Injury | 13% |

| Neck & Shoulder Pain | 8% |

Product Assessment Framework

The integrated assessment evaluated OTC topical pain relief solutions across five critical dimensions.

| Assessment Parameter | Weightage |

|---|---|

| Clinical Effectiveness | 30% |

| Consumer Safety | 20% |

| Ease of Use | 15% |

| Market Acceptance | 20% |

| Innovation Potential | 15% |

Key Active Ingredients Assessment

Topical OTC pain relief products commonly include:

| Ingredient | Primary Function | Consumer Acceptance |

|---|---|---|

| Menthol | Cooling analgesic effect | High |

| Diclofenac | Anti-inflammatory relief | Very High |

| Capsaicin | Neuropathic pain reduction | Moderate |

| Camphor | Counter-irritant action | High |

| Methyl Salicylate | Deep heat relief | High |

Clinical evidence indicates diclofenac topical gel remains one of the most effective OTC topical anti-inflammatory agents for arthritis pain management.

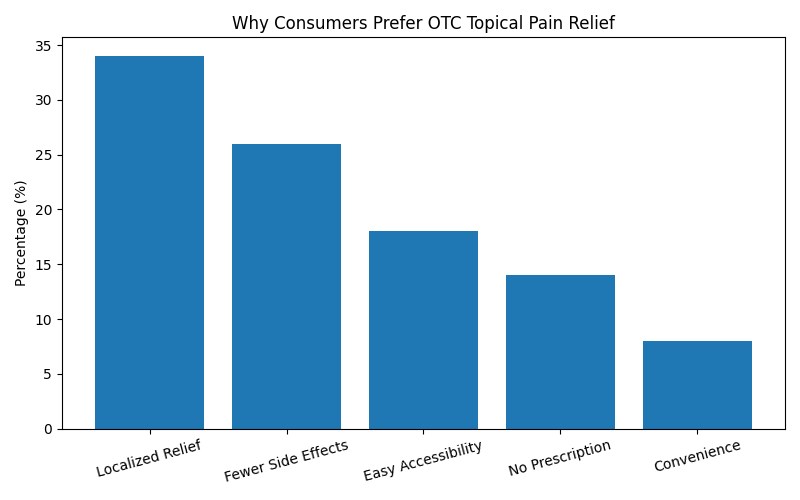

Consumer Preference Analysis

Why Consumers Prefer Topical OTC Pain Relief

| Reason | Response Rate |

|---|---|

| Faster Localized Relief | 34% |

| Fewer Side Effects | 26% |

| Easy Accessibility | 18% |

| No Prescription Required | 14% |

| Better Daily Convenience | 8% |

Consumer Preference Graph

Regional Market Insights

North America currently dominates the OTC topical pain relief segment due to high healthcare spending and strong OTC penetration. However, Asia-Pacific is emerging as the fastest-growing region because of increasing self-care adoption and retail expansion.

Regional Market Share Forecast

| Region | Estimated Share |

|---|---|

| North America | 42% |

| Europe | 26% |

| Asia-Pacific | 22% |

| Latin America | 6% |

| Middle East & Africa | 4% |

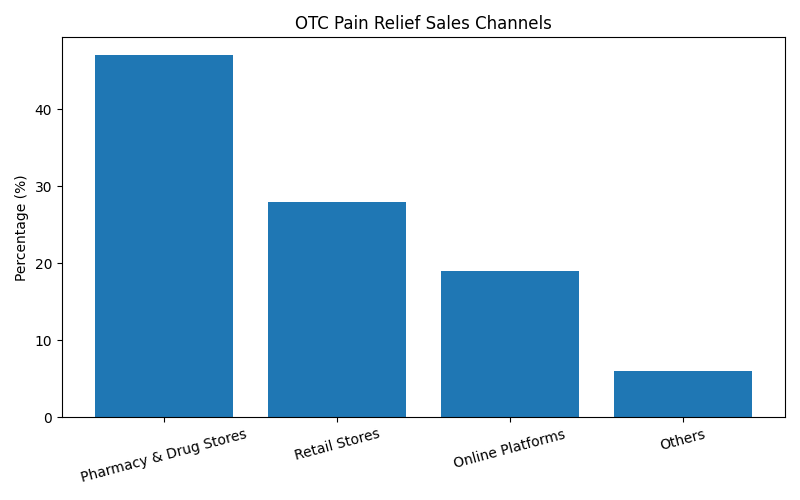

Distribution Channel Analysis

Pharmacies and drug stores remain the dominant channel for OTC topical pain relief products, while online healthcare retail is the fastest-growing segment.

Sales Channel Share

Innovation Trends

The topical pain relief industry is evolving rapidly with advancements in:

- Transdermal delivery systems

- Controlled-release patches

- Herbal & plant-based formulations

- Enhanced absorption technology

- Combination analgesic therapy

- Smart packaging & digital healthcare integration

Patch formulations are expected to become one of the fastest-growing product categories due to extended-release benefits and consistent dosing capability.

SWOT Analysis

| Strengths | Weaknesses |

|---|---|

| Strong OTC demand | Skin irritation risk |

| Rapid localized action | Limited penetration depth |

| Fewer systemic effects | Variable efficacy among users |

| High consumer convenience | Strong market competition |

| Opportunities | Threats |

|---|---|

| Growth in aging population | Regulatory changes |

| Expansion in emerging markets | Generic competition |

| Digital pharmacy growth | Price sensitivity |

| Sports medicine demand | Consumer skepticism |

Conclusion

The OTC topical pain relief segment represents a robust and expanding healthcare category supported by rising chronic pain prevalence, consumer preference for localized therapy, and increasing self-care adoption. Muscle and joint pain solutions are expected to remain a core driver of category growth over the next decade.

An integrated assessment of market trends, clinical efficacy, consumer behavior, and commercial scalability confirms that OTC topical pain relief solutions hold substantial long-term potential for manufacturers, healthcare brands, and global distributors.

With continuous innovation, strong retail penetration, and growing healthcare awareness, topical pain management products are positioned to become one of the most sustainable OTC wellness categories worldwide.

Get Full Case Study

Enter deatils to get full case study.